|

Dear Colleague:

Three years ago, four high roller gamblers – IBM, HP, EMC,

and CA – stepped from their black limousines outside a Las

Vegas casino and were escorted to a velvet-draped poker

room.

Their mission: to see which player would take away the

richest prize in the service assurance software business.

Yes, we’ve glamorized the story a bit, but the money spent

by the IT giants to acquire assurance software brands raised

many eyebrows at the time. CA bought Concord Communications for $350

million. EMC took Smarts for $260 million. HP snagged

Peregrine for $425 million. IBM upped the ante to $800 million to

own Micromuse. And we’ve

only mentioned the biggest of the acquisitions.

Now none of the assurance companies acquired was a pure

telecom play. They all had significant enterprise assurance

businesses. Still, the telecom market was half of Concord’s

and half of Micromuse’s annual revenue.

Yet three years later, one wonders what all the excitement

was about.

In telecom, fault and traditional performance management are no longer the hot

categories they once were. In fact, it’s hard to

find much new about these solutions on the telecom pages of

the IT giants' websites. For the most part, those solutions are

being promoted today as enterprise, not telecom solutions.

Now we think this turn of events says a lot about the

character of today’s telecom assurance market:

The gulf between enterprise and telecom assurance

solutions is widening. The QoS demands of 3G+ and

large-scale IP networks and services are truly advanced

and require an extraordinary level of software

innovation and telecom-specific expertise.

Not only are the technical requirements more rigorous,

the telecom industry also needs to respond quicker to the

latest communications developments.

For instance, eighteen months ago, the 3G data services market was a

sleeper. Then along came the Apple iPod and KABOOM -- things

started to get interesting real fast.

Now suddenly, there was a big need to monitor all sorts of

software applications on a smart phone. The radio network

needed to be optimized as well so that high speed music

downloads didn't cripple voice service.

Network management, then, is telecom's ticket to tomorrow.

Telecoms desperately need the latest network assurance and

service assurance innovations if they hope to continue

offering highly complex services and a high quality customer

experience at the same time.

Trouble is, the telecom assurance software market is

evolving so quickly that the critical assurance sectors –

and the applications where software value amasses – are shifting

dramatically.

But what assurance areas are the most critical today? And

which vendors provide the best solutions to assure telecom's

future?

Well, getting answers to such questions is the purpose of a

new TRI research report, The Telecom Network/Service Assurance

& Remote Test Software Market.

Overall, the

218-page report finds the assurance software market reached

$2.4 billion in 2008 and predicts it will grow to $2.9

billion in 2013.

The Report analyzes this dynamic market and shows how you and your

company can find profitable solutions, invest safely, and/or

avoid excursions into market sectors that are either too competitive or too

specialized to attract enough paying customers.

Opportunities exist across a diverse spectrum of

assurance and test solutions. But where can your company make a difference? Well,

here are some highlights of our analysis to provide some

perspective:

- The Rise of Application Performance Management

- Two and a half years ago a French mobile operator

advertised its very popular mobile data service as “1

Mbps bandwidth for 15 Euros a month”. Today that same

operator offers mobile data service without telling you

what the bandwidth is. The user gets a mixture of

internet access, video on demand, voice mail, and an

email application.

In other words, bandwidth is no longer the issue – the

carrier sells strictly on the types of services and

applications that come in the mobile package.

It's a dramatic break with the past and a key reason

wireless application performance management (APM) has

become critical for operators. The report explains the details behind APM,

the differences between monitoring synthetic vs. real

transactions, and which vendors lead the market.

- Deep Packet Inspection and Complex Services -

What do you do when your network application operates

across multiple network layers and has millions of

possible points of failure? Often the only way to

diagnose problems in an environment like that is to

replicate that application and painstakingly investigate

the problem off-line.

This is the purpose of deep packet inspection assurance

(DPI) solutions that capture all packets passing a

segment of the network and load them into massive data

storage. The report examines the benefits and

kinds of applications that especially lend themselves to

DPI analysis.

- Device Management is Skyrocketing in Importance

because smartphones and mobile data services are

expanding greatly.

Device management solutions help operators sort out

terminal software compatibility problems. They also

track the performance of different types of handsets to

determine which handsets drive traffic and which devices

create more problems than they are worth.

Here the study probes the intriguing market related

questions that mobile assurance solutions can help

answer. In addition, the report looks at the brand

new area of home device monitoring. It explains

what this market is all about, why the rise of femto

cells may be crucial to it, and which vendors are

delivering software solutions.

- Advanced Policy Compliant SLAs - The kind of

service level agreements (SLAs) that make sense for

enterprise customers today go way beyond the traditional

assuring of network connectivity and IP network

performance.

Managing enterprise compliance with “policy assurance”

is the new solution frontier. The idea is to wrap an

enterprise’s full set of operational, security,

regulatory, and industry policies in one over-arching

management framework.

Now BT is the first tier 1 carrier to offer this

innovative policy assurance as a service to its

enterprise customers. When BT sells telecom services to

a healthcare organization, it not only guarantees

network performance, but also "proves" that patient

record confidentiality hasn’t been compromised across

that network.The report explains what's

behind this new policy assurance category, what

technological hurdles needed to be overcome, and how

IP network reconciliation and service orchestration are an

integral part of the solution.

-

Radio Network Optimization - 3G

networks are monitored quite differently than 2G.

3G adds a new access component, the RNC or radio network

controller, which controls: QoS, authentication,

handling weak transmissions, scheduling, and the

prioritization of various services. It’s a dramatic

change for operators who used to handle those processes

in the mobile core.

As you move to 3.5G such as HSPA and 4G in LTE and WiMax,

functionality moves even further out into the edge --

from the RNC to the individual base stations.

The report profiles a new radio

optimization solution that addresses the immense

complexity of these new 3.5G and 4G QoS. issues.

Mapping QoS hotspots within 100 to 200 meters, the

solution offers significant OPEX improvements over

traditional drive test optimization.

The report highlights the key issues in advanced

wireless network QoS, showing where test/QoS solutions

are lacking and which vendors are stepping in to help.

The highlights above are just a sampling of the many

diverse developments and telecom assurance innovations that

are profiled in this market study.

Whether you're a carrier executive aiming to improve your

network/service assurance infrastructure or a vendor delivering

assurance and related solutions, the Report will help you discover:

- What are the most important market

priorities?. . .

- Which success strategies

of other operators can you adopt at your own

telecom organization?

- Which vendors have industry

market share and are leading in specific niches?. . .

- Which OSS players have the right background and market

experience to partner

with?. . .

- What emerging trends

can

your company capitalize on?. . .

Please scan the full table of

contents below. You'll see why this report delivers the

tactical and strategic information you need to fully

understand where telecom assurance and test

are headed.

To access this market intelligence today, contact me at

TRI's

offices at +1-570-620-2320.

Sincerely,

Dan Baker

Research Director, TRI

P.S. This Report is one research module in

TRI's on-going OSS/BSS

KnowledgeBase covering the breadth of telecom

software and OSS innovations.

Table

of Contents

The Telecom

Network/Service Assurance

& Remote Test Software Market

A. EXECUTIVE SUMMARY (2 pages)

B. MARKET VISION (2 pages)

1. Circuit Reliability in a Dynamic IP Telecom World

C. DEFINITION OF TERMS (1 page)

D. PERFORMANCE MANAGEMENT (4 pages)

1. The Virtues of Performance vs. Fault Management

2. Performance Management Overview

3. Marrying Probes with Performance Management

4. The Demand for Better & Faster Customer Reporting

5. PM's Key Capabilities

6. Performance Management Consolidation

E. APPLICATIONS PERFORMANCE MANAGEMENT (5 pages)

1. Why Application Monitoring is Essential in Wireless

2. Application Performance vs. IP Performance Assurance

3. Monitoring Synthetic vs. Real Transactions

4. Monitoring Multiple Java and .Net Transactions

5. Application Management - Mobile Data Applications

6. A Carrier Delivered Solutions for Enterprises

7. Assurance Where Wireless Service is Mission Critical

F. DEEP PACKET INSPECTION SURVEILLANCE (1 page)

1. Combining Deep Packet Inspection and Massive Data Storage

G. FAULT MANAGEMENT & ROOT CAUSE ANALYSIS (4

pages)

1. Fault Management Functions

2. Why EMSs Are Not Sufficient for Fault Analysis

3. The Consequences of Poor Root Cause Analysis

4. Interconnect Fault Management at AT&T Mobilty

5. Intelligent Filtering & Alarm Consolidation

6. Correlation by Network Management Consolidation

7. The Expert Systems Approach to Fault Correlation

8. The Diagnostic or Code Book Approach

9. Limitations of the Code Book

H. CUSTOMER EXPERIENCE & SQM (7 pages)

1. Customer Experience vs. SQM: Definitions

2. Integrating Across Multi-Vendor, Multi-Technology,

Multi-Layer

3. The Challenge of Monitoring a Service's Quality

4. The Benefits of Customer Experience Management & SQM

5. SQM and Service Modeling Example: an MMS Service

6. Service Management -- Provisioning vs. Assurance

Differences

7. Migration of OSS Systems via Federation

8. Creating Enterprise Bundles with the Service Model

9. Gaining Multiple Views of Quality

I. MOBILE DEVICE & HOME NETWORK MONITORING (3

pages)

1. Wireless Device Management

2. Home Monitoring - Advent of Residential Network Assurance

3. Relieving the Call Center from Excess Network Trouble

Calls

J. SLA MONITORING (2 pages)

1. The Components of Service Level Agreements

2. Verifiers Aid the Detection of IP SLA Violations

3. Measuring Service Quality in Wireless

K. SIGNALING ANALYSIS SYSTEMS (4 pages)

1. Signaling Impact on Service Assurance

2. Signaling vs. Performance Management Assurance

3. Voice Quality Analysis

4. Real-Time Analytics & Dynamic Thresholding

5. Service Assurance for Mobile Operators

L. RADIO NETWORK OPTIMIZATION (3 pages)

1. Why VoIP over Mobile Strikes Fear in Operator Hearts

2. The Challenge of HSPA and LTE Deployments

3. Why the Change from 3G to 3.5G and 4G is a Big Quality

Issue

4. Testing Advanced Wireless Networks

5. Where the OPEX Savings Come From

M. REMOTE TESTING & MONITORING (6 pages)

1. Pre-Service Test - Its Unique Value for Operators

2. The Operationalizing of Test

3. Doing More With Moderately Skilled Technicians

4. Key Markets for Remote Test Vendors

5. Multi-Vendor Test: The Virtues of Best Practices R&D

6. Active vs. Passive Testing

7. The Progression of Test: From Lab to Live Network

8. The Advantages Test Vendors have in OSS

N. IPTV SERVICE ASSURANCE (6 pages)

1. The IPTV Monitoring Business

2. The Dispatch Problems That Surround IPTV Services

3. Assuring IPTV Network Capacity

4. What It Takes to Excel in IPTV Assurance

5. Quality of Service and Trouble Management

6. Interconnect Assurance

7. Video Quality Monitoring

8. Technician Coordination with Network Assurance

9. Video Set Top Monitoring

O. CONTROL PLANE & LARGE SCALE IP SOLUTIONS (9

pages)

1. The Rise of the Deep Network Knowledge Guys in OSS

2. Carrier Ethernet - Assurance Spells the Difference

3. From OAM&P to OSS

4. The Challenge of Multi-Vendor Network Control

5. Network Reconciliation - Another Use of the Control Plane

6. Orchestrating Provisioning & Assurance on a Large Scale

7. Policy Assurance - Evolving Telecom Business with

Enterprises

8. BT: Taking Compliance Responsibility for Customers

P. OSS CONSOLIDATION (2 pages)

1. The Consolidation of OSS Systems and Processes

2. The Genius of Micromuse: Manager of Managers

3. Consolidation of the Wireline Work Center

Q. MERGERS & ACQUISITIONS (2 pages)

1. Looking Back: The Mega-Mergers in the Assurance Business

2. How to Manage a Test Company

R. MARKET THREATS (2 pages)

1. The Challenging Life of Assurance Software & Test Vendors

2. An OSS Software Company that Spread Itself Too Thin

S. VENDOR OPPORTUNITIES (6 pages)

1. Where the Telecom Market & Assurance Solutions Will Grow

2. Assessment of Assurance Software Sectors

a. OSS Automation to Drive OPEX Savings

b. Customer Experience Management & SQM

c. OSS Consolidation -- Assurance & Modeling Middleware

d. Large Scale IP Network Assurance & Policy Compliance

e. IPTV Remote Test

f. Deep Packet Inspection Surveillance

g. Home Network Monitoring

h. IP Performance Management Software

i. Fault Management

j. Wireless Radio Network Testing

3. Working Successfully with SIs

T. CARRIER RECOMMENDATIONS (3 pages)

U. MARKET SEGMENTATION & FORECAST ANALYSIS (10

pages)

1. How TRI Develops its Market Segmentations

2. Market Growth Forecast

3. OEM vs. Service Provider

4. Distribution Channels

5. Geographic Region

6. Service Provider Type

7. Service Provider Size

8. Type of Network/Service Assurance or Remote Testing

Solution

9. Networks/Devices Assured

V. VENDOR PROFILES (128 pages)

1.

Alcatel-Lucent

2.

Anritsu

3.

CA Wily

4.

Hewlett Packard (HP)

5.

IBM

6. InfoVista

7. Intelliden

8.

JDSU

9. NetScout

10.

Nokia Siemens Networks

11 Objective Systems

Integrators (OSI)

12. Soapstone

Networks

13. Spirent

Communications

14. Suntech

15.

Tektronix

16.

Telcordia

Vendor

Profiles & SWOT Analysis

TRI's vendor profiles section delivers a detailed

analytical

snapshot of the leading billing companies. Sixteen of

the leading software vendors and network equipment providers

are profiled in the report.

Each of the profiles are between 8 and 10 pages in

length

and are presented in the following sections:

1. Company Specifications and Web Links

This upfront backgrounder information in each profile is

organized in the same format for easy cross-reference in

other profiles.

Here you'll find basic company data organized for

fast retrieval and web access such as:

- Corporate backgrounder

- Overall OSS/BSS business

- Significant investors and stock market reference for

public firms

- Significant customers

- Major vendor partnerships

- Major worldwide locations

- Summaries of key products in the billing market

-

Number of employees

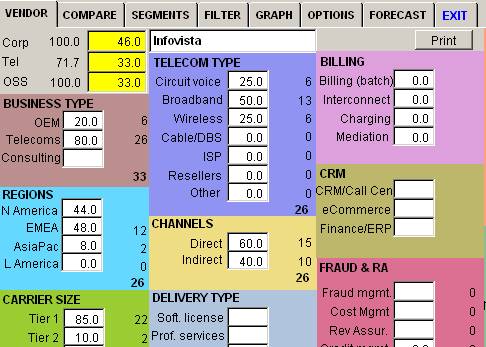

2. Company Revenue & Market Breakdowns

In this section, we provide an estimate of each company's

individual revenue breakdown in the assurance/test market.

The numbers are gathered from public documents,

conversations with people at the companies themselves, and

Dittberner's experience tracking the market since 1997.

Many companies provided guidance on their own numbers.

Here are the segments we breakdown for each company:

- Overall Market Revenues

- Corporate, Telecom Industry & OSS/BSS Revenues

- Business type

- OEM software, Telecoms software, Consulting/SI services

- Channels of Distribution

- Direct, Indirect

- Service Provider Type

- Circuit wireline, Broadband, Wireless, Cable/DBS, Virtual

Network Operator/Non-Facilities Operator, Other

- Size of Carrier

- Tier 1 (>$10 bill. revenue), Tier 2 ($250 mill. to

$10 bill.), Tier 3 (<$250 million)

- Geographic Region

- North America, EMEA, Asia Pacific, Latin America

- Software Delivery Method

- Software License, Prof. Services, Service

bureau/Hosted

- Network/Service Assurance & Remote Test Applications

- Fault management & analysis

- Performance management & analysis

- Service quality, SLA & customer experience management

- Network optimization

- Policy compliance & IP reconcilation

- Remote test

- Trouble/incident management

- Application performance management

- Type of Network/Device Assured/Remote Tested

-

Radio Access Networks|

- ATM/Frame Networks

- Broadband Networks

- Transmission Networks

- Fixed or Mobile Core TDM & Mobile HLR

- IP & Corporate Networks

- Service Delivery & IN Machinery

- Mobile, CPE & Home Terminals

- Other Networks/Devices

This calendar year 2008 data is made further accessible

in a a database

program (delivered as free software with the text report)

that allows you to create instant tables and graphs,

compare various company market shares across these segments,

and produce a variety of reports in Excel format.

Prior year data is also provided on the OSS/BSS market for historical analysis.

3. Dittberner Discussion of Company and SWOT Analysis

You'll no doubt find this section the most valuable

because it's here where each company's assurance business is

put into context. In this section, TRI gets into a

free wheeling discussion on company success

stories, challenges, and significant product developments.

In this discussion, we meander quite a bit on the significance of

company histories, new product/marketing initiatives,

telecom customers, geographic markets, and competitive

forces.

The section concludes with a company Strengths,

Weaknesses, Opportunities, and Threats (SWOT) analysis -- a

candid Dittberner opinion on where each vendor stands

against its competitors and the suitability of its products

and services for the network/service assurance market.

TRI's competitive analysis draws from significant

research such as attending OSS conferences and speaking with

OSS experts at telecoms. We also held 30-minute or

longer conversations with executives at all of the assurance companies we profiled for this report.

Getting so many assurance vendors to participate was an

invaluable aid to the research effort because TRI got to

hear how each company interpreted its role in the

marketplace. In turn, TRI could discuss competitive issues, evaluate trends, and gain

insights on the company's strategy.

When TRI finished its profiles, it also gave companies a chance to check the profile for accuracy and

comment on TRI's analysis.

In all, we think our research methodology meets the twin

goals of: maximizing competitive insights; and

maintaining a relationship of trust with the sources of this

valuable information.

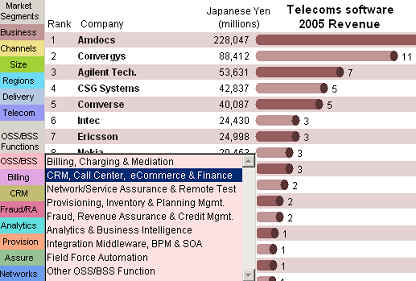

Market

Segments & Forecasts

TRI has also sized and forecasted the worldwide

market for the network and service assurance software market in this

report. Our forecast model is based on several

parameters: TRI's historical tracking of the OSS/BSS

market; TRI's forecast of Next Generation Network

(NGN) services growth; discussions with carrier experts; and

interviews with software and consulting vendors.

The forecast use 2008 as the base year and provide

forecast numbers to 2013. The segments forecasted are

the breakouts described in the Vendor revenue breakouts

above.

* * * * *

Desktop Database and

Search Software

Included in your report

order is a delivers a fully

organized body of knowledge and analysis across two

interfaces:

- Full Report in HTML

Help format for searching the text and

visuals of our analysis modules, case studies, and

vendor profiles, and

- A desktop Software Application

(written in Microsoft Visual Foxpro) with market

segmentation and forecast data that you use to view

customized data tables, graphs, vendor comparisons, and

print documents. Note: all data and forecast

tables are also provided in Microsoft Excel and

comma delimited files can be created too.

Below are some sample screens (NOTE: the examples show

non-revenue assurance and non-fraud companies)

Search

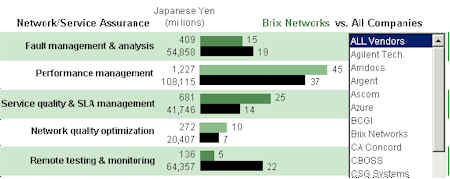

analysis in On-Line Database. . .

Compare

vendor market strength. . .

View,

modify, and print our estimates of company financials. . .

View

market share graphs in international currencies. . .

Technology Research Institute (TRI)

4-25 Rocky Mountain Drive North

Effort of the Poconos, PA 18330

Tel: 570-620-2320

|